The information in this blog is for general informational purposes only and does not constitute legal advice. Consult a qualified attorney for advice on your specific situation. We make no guarantees about the accuracy or completeness of the information provided. Reliance on any information in this blog is at your own risk.

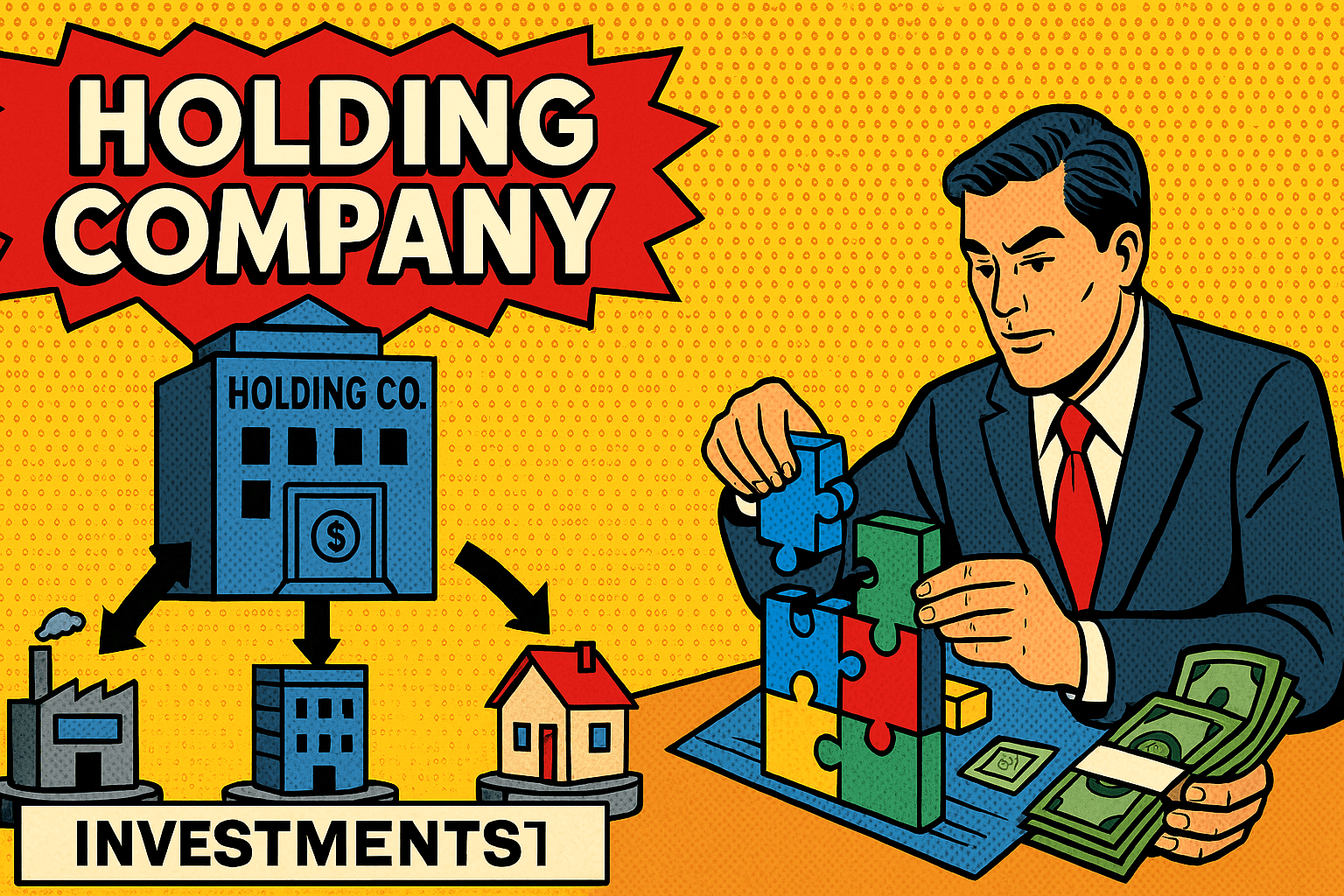

Successful investors understand that how you hold an asset can be as important as which asset you hold. In Ontario, the workhorse for efficient ownership is the holding company—a corporation whose primary job is to own shares or other investments rather than operate a day-to-day business. By inserting a holding company (“Holdco”) between you and your portfolio companies, you can manage liability, streamline tax strategy, and simplify future estate or exit planning.

This post explains how holding companies work under Ontario law, why they are so popular with private investors, and the compliance details you need to get right from day one.

What Is a Holding Company?

Legally, a Holdco is just a regular corporation incorporated under the Business Corporations Act (Ontario) or federally under the Canada Business Corporations Act. The distinction is functional: it does not carry on an active business of its own; instead, it owns shares, partnership units, real estate, or intellectual-property royalties.

Think of Holdco as a personal investment “vault” with its own legal and tax identity. You, your family trust, or your operating business can own Holdco’s shares; Holdco, in turn, owns the assets that fuel long-term growth.

Core Advantages of a Holding Company

1. Liability Containment

When you invest personally, any claim that pierces the target company’s shield could reach your personal assets. Holding shares through Holdco creates an additional corporate veil: creditors of the portfolio company must first pierce that entity, then Holdco, before touching you. While veil-piercing is rare, a double layer adds peace of mind.

2. Tax Efficiency

- Tax-Free Inter-Corporate Dividends – Dividends paid from an active Canadian-controlled private corporation (CCPC) to a connected Holdco generally flow tax-free, preserving cash for reinvestment or debt repayment inside Holdco.

– - Income Splitting (where permissible) – Shares of Holdco can be issued to family trusts or adult family members, allowing dividends to flow to lower-bracket taxpayers, subject to the tax-on-split-income (TOSI) rules.

– - Capital Gains Deferral – Selling an operating company to Holdco via a “section 85 rollover” defers capital-gains tax, freeing funds for future deals.

– - Lifetime Capital Gains Exemption (LCGE) – Shares of Holdco can qualify if 90 percent of its assets are active-business shares at the time of sale and 50 percent for the preceding 24 months. Proper asset “purification” is easier when you use Holdco as a staging vehicle.

3. Reinvestment Flexibility

Because tax-free dividends pile up inside Holdco, it can make follow-on investments, purchase life-insurance policies, or lend to an operating subsidiary—all without triggering personal tax each time cash moves.

4. Estate and Succession Planning

Freezing the value of your common shares in Holdco today and issuing new growth shares to a family trust can lock in the current tax cost while allowing future upside to accrue to the next generation. Holdco also simplifies probate: instead of managing multiple share certificates on death, your estate deals with one entity holding them all.

Typical Holding-Company Structures

- Individual ➔ Holdco ➔ Portfolio Companies

The classic stack. Dividends and gains rise to Holdco, which pays you personally only when needed.

– - Operating Company ➔ Holdco

You create Holdco to own excess cash from Opco, protecting retained earnings from trade creditors and enabling tax-free inter-corporate dividends.

– - Family Trust ➔ Holdco ➔ Investments

A discretionary trust becomes the shareholder of Holdco, allowing income splitting among beneficiaries and facilitating multiplication of the LCGE on an eventual sale.

Setting Up a Holdco Correctly

- Choose Jurisdiction – Ontario incorporation works for most domestic investors; federal incorporation can aid cross-Canada name protection and extra-provincial expansion.

– - Name and NUANS Search – Even numbered corporations need a quick NUANS search to avoid conflicts.

– - Share Structure – Create at least two classes: voting common shares (for control) and non-voting preferred shares (for estate freezes or financing). Future flexibility is invaluable.

– - Section 85 Rollover (If Contributing Existing Shares) – File the proper election within the CRA deadline to avoid an immediate capital-gains hit.

– - Minute Book and Resolutions – Maintain director and shareholder resolutions, share certificates, and registers from day one; missing documents complicate future diligence or sale.

Ongoing Compliance and Reporting

Holdcos enjoy a light operational footprint, but they are not “set-and-forget” vehicles:

- Annual Corporate Filings – Ontario Form 1 or federal annual return plus corporate tax return (T2).

– - Passive-Income Tracking – Once passive investment income in associated companies exceeds $50,000, the CCPC small-business deduction erodes. Monitor combined passive earnings to avoid an unexpected corporate-tax spike in your operating businesses.

– - Part IV Tax – Inter-corporate dividends from non-connect corporations (less than 10 percent ownership) may trigger refundable Part IV tax, tying up cash until dividends are paid out to shareholders.

– - TOSI Vigilance – Splitting income with family members through Holdco demands careful review of the “excluded-business” and “excluded-share” carve-outs.–

Common Pitfalls (and How to Avoid Them)

- Debt Overhang – Borrowing within Holdco to fund investments can be smart, but interest deductibility and thin-capitalization rules require arm’s-length terms and documentation.

– - Commingling Personal and Corporate Funds – Treat Holdco as a separate person: separate bank accounts, bookkeeping, and resolutions for each major decision keep the liability veil intact.

– - Forgetful Annual Meetings – Failure to elect directors or approve financials can invite penalties and complicate future financings.

– - LCGE Purification Left Too Late – If Holdco accumulates passive assets (cash, portfolio securities) beyond permissible thresholds before a sale, shareholders may lose up to $1 million in tax-free gains. Regular “spring-cleaning” transfers surplus assets to an investment subsidiary.–

Case Study: A Two-Company Exit

Situation

Maria and Jason own 100 percent of TechOpco Inc., a software firm worth $8 million. They also have a Holdco that accumulates after-tax profits via inter-corporate dividends.

–

Challenge

A U.S. buyer offers $10 million for TechOpco. Maria and Jason want to access the LCGE, but passive assets inside Holdco now exceed 10 percent of total assets, jeopardising qualification.

–

Solution

Six months before closing, AMAR-VR LAW coordinates with tax advisers to “purify” Holdco: surplus cash moves to an investment subsidiary for a note, and marketable securities transfer under a tax-deferred rollover. At closing, Maria and Jason each claim the LCGE, saving roughly $500,000 in tax per shareholder.

How AMAR-VR LAW Can Support

Holding-company benefits flow only when structure, contracts, and compliance line up. Our firm assists Ontario investors by:

- Incorporating Holdcos with flexible share-class design and robust minute-book preparation.

– - Drafting Inter-Corporate Agreements—loan, management-fee, or royalty contracts—that stand up to CRA scrutiny.

– - Coordinating Estate Freezes with accountants to lock in tax cost and multiply LCGE eligibility.

– - Reviewing Passive-Income Exposure and advising on purification strategies well ahead of an exit.

We blend corporate, tax, and securities insight so your holding-company plan is both practical and legally durable.

Conclusion

A holding company is not just a shell; it is a versatile platform for controlling liability, clawing back tax otherwise lost, and paving smooth paths for succession or sale. But those advantages are not automatic. They depend on early-stage design—clear share classes, proper rollovers, airtight governance—and ongoing vigilance over passive income, corporate filings, and documentation.

–

Contact us today for a consultation if you are considering a holding company or need to optimise one you already have. We’ll help you build, maintain, and leverage a Holdco that keeps more money compounding under your control—while keeping unnecessary risk where it belongs: outside your balance sheet.

Frequently Asked Questions (FAQs)

- What is a holding company and how does it differ from an operating company?

–

A holding company is a corporation formed primarily to own shares, investments, or other assets, rather than operate a business. In Ontario, it is legally identical to an operating company in structure, but functionally serves as an investment and liability shield rather than a day-to-day enterprise.

– - What are the main advantages of using a holding company for private investments?

–

Holding companies offer liability protection, tax efficiency through inter-corporate dividends, reinvestment flexibility, and simplified estate and succession planning. They also enable capital-gains deferrals and better control over Lifetime Capital Gains Exemption eligibility.

– - Are there risks or compliance issues investors should watch for with Holdcos?

–

Yes. Passive income exceeding $50,000 across associated companies can erode the small-business deduction. Failing to observe corporate formalities, track passive-asset thresholds, or file timely returns may lead to tax penalties, loss of LCGE eligibility, or weakened liability protection.

– - How does a holding company affect access to the Lifetime Capital Gains Exemption?

–

Shares of a holding company can qualify for the LCGE if the business assets held meet active-business thresholds both at the time of sale and during the prior 24 months. Timely “purification” is often necessary to remove excess passive assets and preserve eligibility.

– - How can AMAR-VR LAW assist with setting up and maintaining a holding company?

–

AMAR-VR LAW helps investors by reviewing subscription documents, assessing exemption compliance, identifying legal risks, and negotiating protections such as pre-emptive rights and exit terms. We ensure your investment is structured legally and aligns with your financial strategy, giving you clarity before you commit.